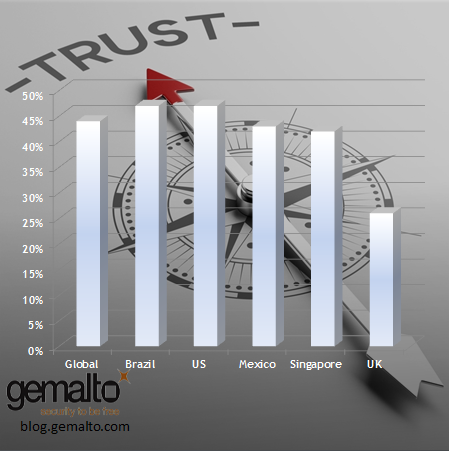

Trust in banks around the world is still tentative, according to the latest Global Consumer Banking Survey from EY. Whilst overall confidence levels are stabilizing, but notably NOT increasing – banks still have a lot of work to do. As this graph, depicting numbers with “complete” trust in their bank, shows…

In the UK alone, 1.6 million people switched bank accounts in 2014, a rise of 12% since 2013. Add to this, the fact that non-financial companies such as Apple, PayPay and Google are entering the financial services market; and you realize that the pressure is on for traditional banks to up their game – particularly with Generation mBanking. Given all the evidence for an appetite for mobile mbanking in the youth market, how can bank use it to improve customer retention and growth?

As our Generation mBanking report explains, financial service leaders should be prioritizing two things:

- Building out the service catalogue and user experience for Generation M, as outlined in one of my previous blog posts.

- Use new techniques and tools to engage and upsell to your upcoming audience, from social media platforms, digital content to intelligent mobile marketing methods

The mobile channel is a cost-effective way to educate and engage people in product offers and marketing content. It allows the right consumers to be targeted at the right time, driving organic growth and customer retention – and ultimately increasing revenue.

Dynamic messaging programs can be used to deliver “tappable” tailored offers and content to the pre-login mobile apps screen. Mobile can also be used to educate customers about digital fraud prevention or share value-added content such as financial guides for first-time homebuyers or parents.

The ROI from this kind of activity is two-fold. First and foremost, mobile channels cost less to serve. According to the TowerGroup, the average cost per transaction of the mobile banking channel in the US is two percent of branch-based transaction costs. And of course the right marketing and advertising campaigns will boost revenues.

But there is also an incredible return from the recognition and excitement that comes from being seen as an innovator by existing and convenient capabilities to customers, particularly Generation M. Adding useful, interactive and convenient capabilities to mobile banking not only boosts the channel’s ROI, but also demonstrates to customers that financial institutions understand their current needs and are working to anticipate their future needs.